DAF Donations

Hi, I was wondering how everyone here gives credit to donors for gifts from their donor-advised fund? Currently, I place the check from the donor-advised fund under their record. However, my supervisor has recently learned that many organizations around the country are giving the company who provided the donor-advised fund the hard credit for the check and then soft crediting the donor. My issue with this is that I’m afraid it will make it more difficult to track our donors’ giving to us in queries. How has everyone else handled these checks? Thanks.

Answers

-

Michael — these are excellent questions to be asking.

There are a few different schools of thought on this, and the most important thing is that your organization develops a policy, documents it, and applies it consistently.

One resource that you may find helpful is @Bill Connors' bbcon presentation from a few years back. Tagging him here so he can share any updated perspectives.In my own work, I’ve used both models:

• hard crediting the donor and soft crediting the DAF, and

• hard crediting the DAF and soft crediting the donors.

There are pros and cons to each approach.Generally speaking, my preference is to hard credit the donor, soft credit the DAF, and then use gift subtypes, gift codes, or attributes to ensure I can report accurately on DAF giving while still receipting and acknowledging appropriately.

Since you’re currently hard crediting the donor, my recommendation — without knowing more about your internal reporting needs — would be to continue with that model and make sure you’re soft crediting and/or using subtypes, gift codes, or attributes to capture any additional information required for reporting.

3 -

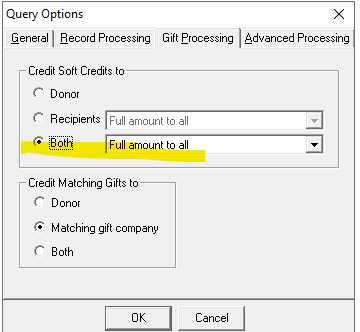

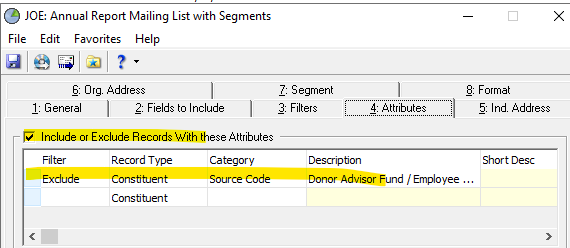

We hard credit the DAVF, since that is where the check is coming from and so does our accounting department and then we soft credit the donor/person. We make sure all of our DAVF's have a code of Donor Advisor Fund. We have a attribute code called Source Code, since we track where the first gift came from, donation, event, Donor Advised Fund, etc. To make sure the donor/person pulls in queries, we choose CREDIT SOFT CREDITS TO BOTH and then include in the filter, source code does not equal Donor Advised Fund. The key is to make sure your Donor Advised Funds are coded as that. You can also exclude these in RE Mail, etc. This all works good for us and we have never had an issue.

4

4 -

Hi! We enter the gift on the donor record and use 'other' as the gift type. Gift type 'other' is only used for DAF gifts. We add an attribute to this gift record with the DAF Company details. We created a gift attribute and under Category section we called this 'alternate payment'. The description section is a table where you can choose or add the DAF company name. This way we only have one record of the donation. We can find the DAF company with an easy query. You could also enter the specific fund name in the comments section. I hope this helps.

0 -

DAF account has own record, linked via relationship to the sponsoring org (the legal donor), and the advisor (the real donor). Allows for automatic soft credit to advisor(s), assigning fundraisers, make the advisor(s) a contact for proper acknowledging, etc.

A million ways to skin this cat. If I was starting from scratch, I would just hard credit the donor and do what Carlene describes. Though the way I currently run is a close second.

1 -

I recommend that you take the course of least disruption. Since your practice is crediting the donor, I'd stay the course and leverage attributes as others have suggested. What you don't what to do is swing the other direction and have a reporting period where gifts before this date were credited to the donor and gifts after were credited to the DAF. This makes for labor intensive reporting for five-ish years depending on how many years your board/annual/monthly reports include. And if the person who understand how to do the reporting leaves and there is no succession plan with the institutional knowledge to generate the reports, you will find yourself with a staffing issue as nobody will want to stay in the role for long.

1 -

Since Carlene tagged me, some notes in addition to what my bbcon presentation says:

- I don't recommend creating a constituent record for the DAF in any situation. The DAF is just an account at a Foundation. Maybe a constituent record for the Foundation, but the DAF itself does not need a constituent record IMHO.

- I actually prefer to hard credit the legal donor and soft credit others. HOWEVER, the worst feature of RE IMHO is Soft Credit output and many, many folks have had problems using RE when data entry has been done that way. Thus the ideas in the presentation that Carlene linked to to HC the "real donor." the person, and maybe soft credit the foundation. We need to use RE how we can get it work for us, not be forced into artificial guidelines that don't actually work with the software we have.

- Consistency is perhaps the most important. Don't suddenly change your procedures on this topic without thinking through long and hard how it affects the past gifts and how you're going to pull outputs (queries, reports, dashboards, etc.) with data entered both ways — and it's not easy to flip flop the hard and soft credits for previous gifts no matter which way you did it before.

This is one of the hardest topics I consult with clients on, thus my point it's the worst feature of RE today. So be patient and thoughtful, it's not an easy topic.

4 -

I do think if you aren't going to hard credit the individual then it makes sense to create DAF account records. Plenty of benefits I've found with doing that.

- Automatic soft credit

- Ability to assign fundraiser (usually as a trailing solicitor type when the individual is assigned)

- Easy receipting with a proper letter type/template

- Less confusing for staff - instead of looking at tons of gifts from different accounts on the one foundation record

- Give them a DAF constituent code to easily exclude or include in reports, queries, etc.

- VSE asks you to report on DAFs by the individual accounts

0 -

Question: If we "hard credit" the donor for DAF pledge payments / DAF outright cash, how would you differentiate these payments when running your Year End Tax Statements? Year End Tax Statements should not include DAF payments since the organization "housing" the DAF already gives them Tax Statement information when the donor funds the DAF.

0 -

I've seen both. A major - but often underappreciated - difficulty with applying the gift to the DAF record is if you ever need to do a data migration. The soft credit connection often doesn't transfer to a new system, and then there is no way to connect the gift back to its donor.

While legally and financially, the funds do belong to the DAF fund, it's important to also remember that our job is in constituent relationship management. Recording to the donor record better facilitates relationship management because it improves functionality with donor giving levels, next ask amount formulas, historical attribution, and forward planning for potential data migrations, exports, and inter-organizational collaboration. Like others, we use the gift subtype to document its DAF source, and we assign a $0 receipt amount to eliminate any potential double-deduction issues.

4 -

Hi Michael,

We hard credit the donor and always include the DAF in the reference field, which is then how I easily query all constituents with DAF gifts over the past FY (or a range of FYs, if & when applicable). Most of our DAF funds (where the check comes from) have stated to not send any acknowledgements to them, so we now rarely soft credit them. We've noticed the soft credit is not as important as the funds coming from the donors themselves per their DAF.

0 -

@Penelope Saruwatari - technically, according to the legal rules for DAFs, they can't be used to pay donor pledges. See this article by the National Philanthropic Trust for a good explanation:

To answer the original question: We are a school and follow CASE Global Reporting Standards, which say that the hard credit goes to the entity with ownership of the money. In the case of DAFs, this is the foundation that houses the DAF for the donor, since they have already given the donor a tax receipt for their donation. So we hard credit the Foundation and soft credit the donor with a "Reference" naming the individual DAF. We then pull all these fields into our acknowledgement letter so it is clear where the money came from. Example: "Thank you for your gift of $xx from the [DAF name] through [Foundation name]"

We also have set up a gift attribute called "Payment Type" where we can indicate it was a DAF payment, and then we can pull reports on it to see which donors use DAFs for specific solicitations.

3 -

Like many others above we hard credit the donor (makes it easy for re-solicitation, recognition etc), we soft credit the foundation (not the individual DAF) since they are the "legal donor", we use a gift type of Donor Advised Fund to help us track which donors have/are using these funds. This gift type could also help with adjusting the gift acknowledgment letters, depending on your current processes. Hope this helps!

0 -

I feel like this may be one of the top 10 most controversial topic in database management! The good news is unless you're part of a group that does have specific rules, there really isn't a "right" answer. No matter who you decide to hard credit or soft credit, just be sure you are consistent and you document your process. (And yes, be sure you're not including the donations in any tax receipting.)

1 -

As most have said, this is a controversial topic with many options.

I took a course YEARS ago from a DAF organization and they suggested that the DAF NEVER have it's own record since the money is really coming to us from the donor, it's just their preferred method of giving. I always hard credit the donor and then I have an attribute for Donor Advised Fund [Jane and John Doe Charitable Fund] and then the DAF Organization [Fidelity, Schwab, etc.] and those pull into the letters. My letters read: Thank you for recommending a distribution of «Amount» to the «Fund_description_1» from the «Donor_Advised_Fund_1» at «DAF_Organization_1». This makes reporting fairly easy because it lives on the donor's record so you have a full picture of their giving history without having to pull soft credits. Just make sure you mark the receipt amount as $0 if you send year end statements, since they've already gotten tax credit from the DAF org.

1 -

I agree with Bill Connors that this has been one of the hardest topics for many years!

For us, we process DAF gifts as organization records rather than directly on the individual's record. This allows us to capture the exact name of the DAF fund and track the true source of the appeal, rather than coding the gift with a generic DAF appeal.

This method has been working well for us. All of the DAF gifts are in organization records tagging it with a primary Constituency Code of “Individual” and “Donor-Advised Fund” as a secondary code, so it gets counted as Individual records on reports. We link DAF record to the individual’s record; we configured the system to automatically soft credit the gift from the DAF’s record to the individual's record. This best practice ensures we don't lose the individual donor's history while accurately reflecting where the money legally originated.

We do this primarily for these reasons:

- A single individual donor may hold multiple Donor Advised Funds (DAFs). By linking the gift to a specific, unique DAF fund record, we avoid confusion if that same donor makes subsequent grants from a different fund.

- Rather than using a generic "DAF appeal" code, we prefer to track the actual source of the appeal (e.g., a specific direct mail piece) that triggered the grant recommendation.

- We want to track the exact, official name of the recommending DAF fund for proper recognition and stewardship.

- Giving the hard credit to the DAF record satisfies finance reports and align with IRS regulations, as the legal donor of the record is the sponsoring foundation.

By linking the DAF fund record back to the individual donor's personal profile, we can set up the system to automatically soft credit the gift to the individual. This ensures the donor's personal giving history remains accurate and they receive proper personal recognition without distorting our hard-credit revenue reporting.

We sometimes do what Joe Moretti mentioned above. You have the option in Raiser’s Edge on choosing whether to credit soft credits to the individual or both, but you need to be careful when choosing both especially for revenue reports. This option can easily lead to double-counting. It’s ideal for recognition, not for financial revenue totals.

I love hearing what others are doing!

0 -

Thank you Everyone!! Lots of great suggestions and the reasoning "behind" these suggestions (that is so important to me). I will definitely consider all of them and work with my team to come up with what will work best for our organization. Thank You Again!!

0

Categories

- All Categories

- New YourCause Community TEST

- New SKY Community TEST

- New Grantmaking TEST Community

- New Altru Test Community

- New bbcon Community - TEST

- 12 Blackbaud Agents for Good™

- New Raiser's Edge NXT Community

- 7 Blackbaud Community Help

- 218 bbcon®

- 1.4K Blackbaud Altru®

- 409 Blackbaud Award Management™ and Blackbaud Stewardship Management™

- 1.2K Blackbaud CRM™ and Blackbaud Internet Solutions™

- 16 donorCentrics®

- 361 Blackbaud eTapestry®

- 2.7K Blackbaud Financial Edge NXT®

- 681 Blackbaud Grantmaking™

- 599 Blackbaud Education Management Solutions for Higher Education

- 3.3K Blackbaud Education Management Solutions for K-12 Schools

- 952 Blackbaud Luminate Online® and Blackbaud TeamRaiser®

- 85 JustGiving® from Blackbaud®

- 7K Blackbaud Raiser's Edge NXT®

- 3.9K SKY Developer

- 257 ResearchPoint™

- 123 Blackbaud Tuition Management™

- 165 Organizational Best Practices

- 247 Member Lounge (Just for Fun)

- 40 Blackbaud Community Challenges

- 37 PowerUp Challenges

- 3 (Closed) PowerUp Challenge: Grid View Batch

- 3 (Closed) PowerUp Challenge: Chat for Blackbaud AI

- 3 (Closed) PowerUp Challenge: Data Health

- 3 (Closed) Raiser's Edge NXT PowerUp Challenge: Product Update Briefing

- 3 (Closed) Raiser's Edge NXT PowerUp Challenge: Standard Reports+

- 3 (Closed) Raiser's Edge NXT PowerUp Challenge: Email Marketing

- 3 (Closed) Raiser's Edge NXT PowerUp Challenge: Gift Management

- 4 (Closed) Raiser's Edge NXT PowerUp Challenge: Event Management

- 3 (Closed) Raiser's Edge NXT PowerUp Challenge: Home Page

- 4 (Closed) Raiser's Edge NXT PowerUp Challenge: Standard Reports

- 4 (Closed) Raiser's Edge NXT PowerUp Challenge: Query

- 822 Community News

- 3.1K Jobs Board

- 57 Blackbaud SKY® Reporting Announcements

- 47 Blackbaud CRM Higher Ed Product Advisory Group (HE PAG)

- 19 Blackbaud CRM Product Advisory Group (BBCRM PAG)